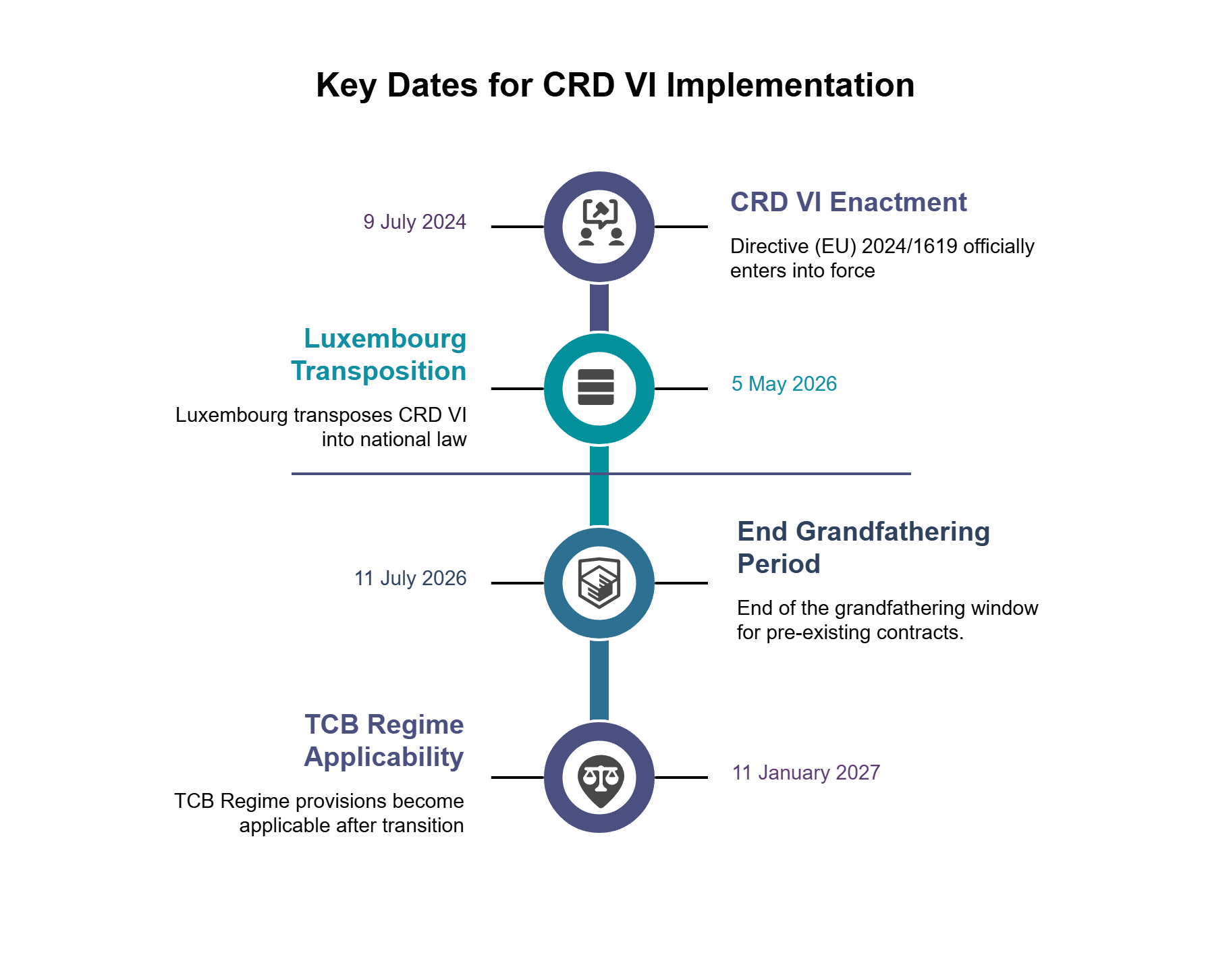

With the expiry of the grandfathering period under Directive (EU) 2024/1619 amending Directive 2013/36/EU as regards supervisory powers, sanctions, third-country branches, and environmental, social and governance risks (the "CRD VI Directive") coming to an end, attention now turns to the Luxembourg implementation of the Third-Country Branch regime (the "TCB Regime").

The law of 5 May 2026 (the "CRD VI Law") transposes the TCB Regime into Luxembourg law, by amending the law of 5 April 1993 on the financial sector (the "LFS"). The TCB Regime will enter into force on 11 January 2027.

Recall of the Luxembourg law status: a permissive regime

Prior to the transposition of the CRD VI Directive, the cross-border provision of banking services by third-country firms and the establishment of their branches in Luxembourg were governed primarily by the LFS and CSSF Circular 11/515.

Under the previous regime, third-country credit institutions wishing to provide banking services in Luxembourg on a permanent basis were authorised by the CSSF and established a branch in Luxembourg pursuant to Article 32 of the LFS.

Separately, Article 32(5) of the LFS allowed third-country firms not established in Luxembourg to provide banking services on an occasional and temporary cross-border basis, subject to prior written CSSF authorisation but without the need to establish a branch. CSSF Circular 11/515 set out the conditions governing this "light-touch" authorisation.

A third path also existed in practice, though it was not expressly articulated in the LFS. Under the framework applicable to investment services, governed by Article 32-1 of the LFS, CSSF Circular 19/716 and CSSF Circular 20/743, a service was deemed to be provided "in Luxembourg" only where the place of its "characteristic performance" (i.e., the essential service for which payment is due) was Luxembourg. Where that condition was not met, no branch requirement or prior authorisation applied. An analogous territorial logic was applied in relation to CSSF Circular 11/515 for banking services, drawing on the European Commission's interpretative communication of 20 June 1997 on the freedom to provide services in the banking sector (97/C 209/04). Under that approach, the mere fact that activities were directed at Luxembourg clients, or that clients were domiciled there, was not in itself sufficient to treat the activity as being carried on within the Luxembourg territory; what mattered was the place where the service was actually performed.

The preparatory works to the CRD VI Law have confirmed this reading. They state that, "in accordance with existing practice", where a banking activity is carried out wholly and exclusively at a distance from a third country with no relevant connecting factor to Luxembourg, it may be regarded as provided outside Luxembourg. This constitutes an acknowledgment of Luxembourg's established administrative practice and confirms that the territoriality of banking services was already assessed on a basis broadly aligned with the characteristic performance test applicable under MiFID II. The new Article 32-3 of the LFS does not seem to depart from this approach.

What happens next?

Article 32(5) LFS has been repealed, along with the specific provisions of Article 32 that formerly applied to third-country credit institutions.

Pursuant to Article 32-3 LFS, third-country undertakings wishing to provide core banking services in Luxembourg will be required to establish an authorised branch and obtain prior authorisation from the CSSF. The CSSF must, before granting authorisation, consult the Luxembourg AML/CFT supervisory authority and obtain written confirmation from it, a requirement not provided for under the CRD VI Directive. The CSSF retains the power to require, on a case-by-case basis, that a third-country branch be converted into a subsidiary. The CSSF may also decide that existing third-country branch authorisations granted no later than 10 January 2027 under the former Article 32 of the LFS remain valid, provided that the branches comply with the requirements of the new framework.

The CRD VI Law reflects both the material and personal scope of the TCB Regime as set out in the CRD VI Directive, together with the main exceptions and limitations to the regime.

TCB Regime scope: art. 32-2 LFS

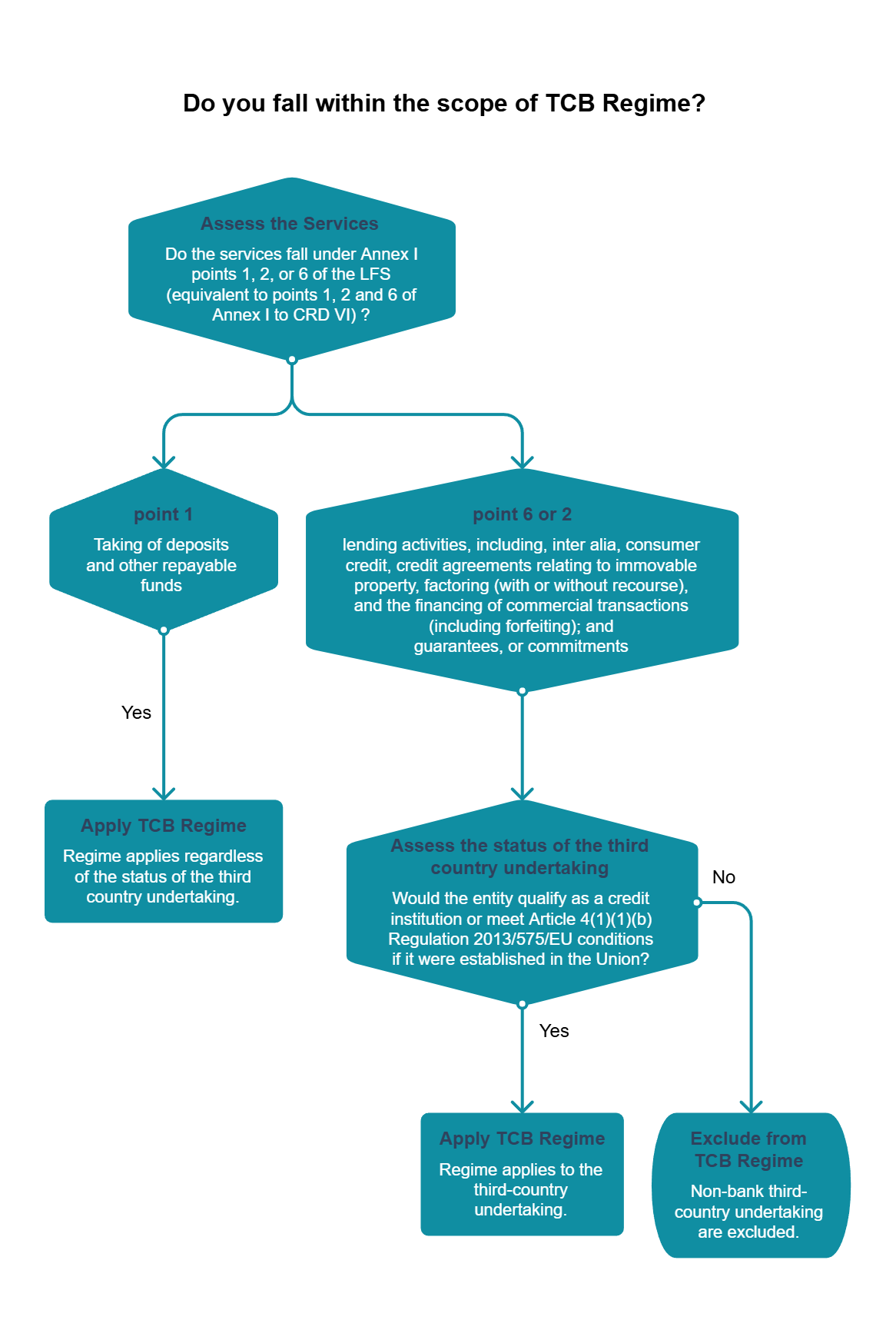

It is necessary to assess, on the one hand, the relevant services that are provided and, on the other hand, the third-country undertaking carrying out those.

Article 32-2 (2) LFS reproduces the MiFID carve-out contained in Article 21c(4) of the CRD VI Directive.

Territorially, the CRD VI Directive does not clarify when a service is considered to be "provided in" a Member State for the purpose of triggering the branch requirement. The new Article 32-3 of the LFS appears to follow the same pre-law of 5 May 2026 territorial approach as mentioned above based on the "characteristic performance" test, under which, where a banking activity is performed entirely remotely from a third country, with no relevant connecting factor to Luxembourg, it may be regarded as provided outside Luxembourg and therefore fall outside the scope of the branch requirement.

Exemptions

Exemptions are set out in Article 32-3 (2) LFS and they are consistent with the CRD VI Directive:

reverse solicitation, the Luxembourg preparatory works clarify that the burden of proof lies squarely on the third-country firm, which must be able to document at all times that the client took the initiative. The CSSF may require group entities established in Luxembourg to provide information to verify genuine reverse solicitation. Whether a new product category is being marketed must be assessed case by case. The reverse solicitation exemption is conceptually uncertain and practically difficult to apply: its key terms are undefined, its interpretation varies across Member States. A critical unresolved question for the loan markets is whether the initiative can be exercised by a third party acting on the borrower's behalf,

interbank operations,

intragroup transactions.

Grandfathering

Consistent with the CRD VI Directive, following Article 73 LFS, the TCB Regime does not apply to contracts entered into before 11 July 2026. Following the parliamentary preparatory works, the stated objective is to "preserve the vested rights of clients under existing contracts". The preparatory works state that "the implementation of the terms of a framework agreement concluded before 11 July 2026 is covered by the derogation". However, the treatment of amendments or restatements and other contractual changes of a pre-11 July 2026 contract remains uncertain.

Conclusion

Luxembourg has transposed the CRD VI TCB Regime largely in line with the CRD VI Directive, subject to a few Luxembourg-specific adjustments including for instance additional AML/CFT involvement in the CSSF authorisation process. The preparatory works also indicate an intention to preserve a certain territorial approach.

Share on