Open-ended AIFs and UCITS must integrate at least two liquidity management tools under the new AIFMD II framework.

Regulatory update – Investment funds

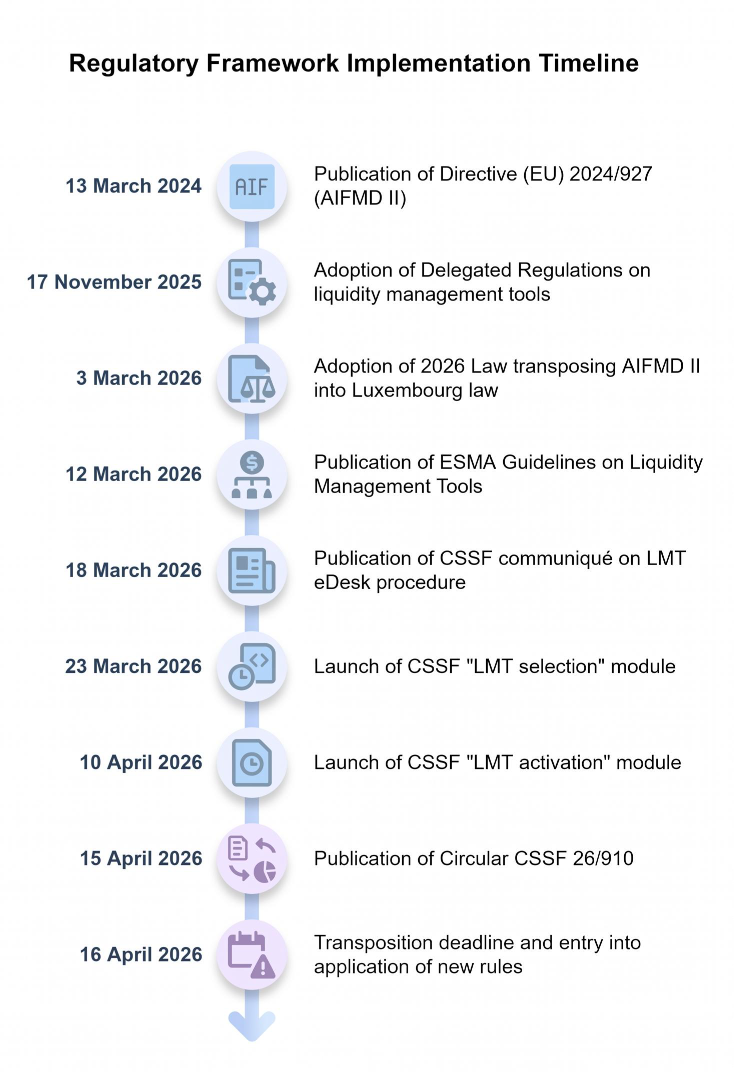

The deadline for the transposition of Directive (EU) 2024/927 (the “AIFMD II”) was 16 April 2026. The European Commission has finalised the regulatory technical standards specifying the operational characteristics of the liquidity management tools (“LMTs”) that will apply to both AIFs and UCITS. In Luxembourg, the transposition has been carried out by the law of 3 March 2026 (the "2026 Law"), amending the law of 17 December 2010 relating to UCIs (the "UCI Law") and the law of 12 July 2013 on AIFMs (the "AIFM Law").

In addition, ESMA published, on 12 March 2026, its Guidelines on Liquidity Management Tools of UCITS and open-ended AIFs (the "ESMA Guidelines"), which the CSSF has integrated into its administrative practice and regulatory approach through Circular CSSF 26/910 dated 15 April 2026 (the "Circular").

Two Delegated Regulations, supplementing AIFMD II and implementing the regulatory technical standards (“RTS”), were published in February 2026:

- Delegated Regulation (EU) 2026/465, specifying the characteristics of LMTs for AIFs;

- Delegated Regulation (EU) 2026/466, specifying equivalent rules for UCITS.

ESMA Guidelines, developed on the basis of Article 16(2h) of the AIFMD, Article 18a(4) of the UCITS Directive and Article 16(1) of the ESMA Regulation, provide guidance on the selection, calibration, activation and deactivation of LMTs by fund managers for liquidity risk management and for mitigating financial stability risks. The Circular confirms that the CSSF, in its capacity as competent authority, applies the ESMA Guidelines with a view to promoting supervisory convergence at European level.

AIFMD II establishes a harmonised European regulatory framework for LMTs, replacing the previously fragmented environment in which the availability and structure of such tools were largely subject to national supervisory practices.

In the Luxembourg context, the reform does not introduce fundamentally new mechanisms. Instead, it formalises and harmonises practices that have already become widely established in the industry, particularly regarding anti-dilution mechanisms and liquidity governance.

The new regulatory framework

The reform is built on three complementary layers.

First, AIFMD II amends the AIFMD and UCITS directives and introduces a harmonised list of LMTs that can be used by fund managers.

Second, the RTS adopted in November 2025 define the technical characteristics and operational conditions of LMTs.

Third, the ESMA Guidelines provide detailed guidance on the selection, calibration, activation and deactivation of LMTs, addressing general principles, quantitative-based tools, anti-dilution tools and side pockets.

The regulatory objective is to ensure that fund managers can effectively manage redemption pressures during periods of market stress, while at the same time ensuring the fair treatment of investors and preserving financial stability.

Mandatory liquidity management toolkit for open-ended AIFs and UCITS

AIFMs managing open-ended AIFs and UCITS are required to select and implement appropriate LMTs for each fund under their management.

In selecting the two mandatory LMTs, the ESMA Guidelines recommend that fund managers consider, where appropriate, whether to select at least one quantitative-based tool (i.e. redemption gates or extension of notice periods) and at least one anti-dilution tool (i.e. redemption fees, swing pricing, dual pricing or anti-dilution levies), taking into account the investment strategy, redemption policy and liquidity profile of the fund as well as the market conditions under which they may be activated. Fund managers may also consider whether to select one tool to use under normal market conditions and one tool to be used under stressed market conditions.

The EU list includes several mechanisms already well known to the Luxembourg market:

- redemption gates

- swing pricing

- anti-dilution levies

- redemption fees

- extension of notice periods

- redemption in kind

- side pockets

Operational rules introduced by the RTS

While the directive establishes the regulatory framework, the RTS define how LMTs operate in practice.

They specify, in particular:

- activation thresholds;

- calculation methodologies;

- investor treatment mechanisms; and

- operational constraints.

While the RTS standardise the functioning of the tools, the overall responsibility for liquidity risk management remains with the AIFM, which must ensure that the tools chosen are appropriate to the fund’s investment strategy, as well as its liquidity profile and redemption terms. In accordance with the ESMA Guidelines, fund managers should be able to demonstrate, at the request of the CSSF, that the activation and calibration of the selected LMTs are in the best interest of all investors and are appropriate and effective in light of market conditions and the relevant characteristics of the fund.

Redemption gates

The RTS require that redemption gates must be triggered by predefined activation thresholds.

For AIFs, these thresholds may be based on:

- a percentage of the fund’s net asset value (“NAV”);

- a monetary threshold;

- a percentage of liquid assets; or

- a combination of these metrics.

The RTS also provide for different gate structures for AIFs, including:

- fund-level gates, which are triggered by aggregate redemption orders;

- investor-level gates, triggered by individual redemption requests; and

- combined gate structures incorporating elements of both approaches.

For UCITS, the framework is more standardised. The activation threshold for redemption gates must be determined at the level of the UCITS and expressed as a percentage of the fund’s NAV, taking into account aggregate redemption orders for a given dealing date or period.

The above provisions encourage managers to adopt a quantitative approach to monitoring liquidity that can identify redemption pressures at an early stage.

Even where the activation threshold is exceeded, the manager retains discretion as to whether to activate the redemption gate, considering the liquidity of the fund, prevailing market conditions and the best interests of investors.

Anti-dilution mechanisms

The RTS also provide detailed rules for anti-dilution LMTs.

These are:

- swing pricing;

- dual pricing;

- anti-dilution levies; and

- redemption fees.

The RTS adopt a broad economic definition of liquidity costs and provide that such costs generated by subscriptions or redemptions should be borne by the investors entering or exiting the fund, covering both explicit transaction costs and implicit costs, such as the market impact cost due to the purchase or sale of assets.

The anti-dilution feature of swing pricing, widely used in Luxembourg funds, is explicitly recognised. The RTS make it clear that the published NAV must reflect the swing factor adjustment, and that both full swing and partial swing methods are acceptable.

For many Luxembourg managers, these rules will therefore formalise existing industry practices rather than introduce entirely new mechanisms.

Suspension mechanisms and side pockets

The RTS also provide clarification on the functioning of some of the tools typically used in stressed market conditions.

Where redemptions are suspended, the suspension must apply simultaneously to subscriptions, repurchases and redemptions.

This ensures that all investors are treated on an equal basis during periods of market disruption.

Side pockets are also recognised as LMTs. They may be created either by:

- accounting segregation within the existing fund; or

- physical separation of affected assets into a distinct structure.

These mechanisms may be particularly useful for funds that invest in illiquid assets or assets that are subject to exceptional valuation uncertainty.

The ESMA Guidelines further emphasise that fund managers should ensure that the level of subscription and redemption orders received is treated in a manner that prevents certain investors from benefiting from information regarding the potential activation of LMTs, for instance where activation thresholds may be reached in the case of redemption gates.

Luxembourg supervisory perspective

In connection with the entry into application of the 2026 Law, the CSSF has launched a dedicated "LMT eDesk procedure" comprising two modules: an "LMT selection" module, through which UCITS, or where applicable their management companies, and authorised AIFMs, are required to communicate their selection of LMTs together with their detailed policies and procedures governing their activation and deactivation; and an "LMT activation" module, through which such entities are required to notify the CSSF of the activation or deactivation of suspensions of subscriptions, repurchases and redemptions, of any LMT used in a manner that is not in the ordinary course of business, and of side pockets.

The information provided through the eDesk procedure will subsequently be used by the CSSF to notify the relevant competent authorities, ESMA and, where applicable, the ESRB, in accordance with the provisions of the UCI Law and the AIFM Law. In addition, Luxembourg-domiciled funds subject to Part II of the UCI Law, specialised investment funds governed by the law of 13 February 2007 and investment companies in risk capital governed by the law of 15 June 2004, which do not qualify as AIFs or are not managed by a Luxembourg-authorised AIFM, are also required to notify the CSSF of the activation or deactivation of suspensions and the creation of side pockets under the "LMT activation" module.

In addition, the Circular recommends that open-ended specialised investment funds not governed by Part II of the Law of 13 February 2007, which are subject to CSSF Regulation Nº 15-07, as well as open-ended UCIs subject to Part II of the UCI Law managed by a registered AIFM, consider the provisions of the Circular in conjunction with Commission Delegated Regulation (EU) 2026/465, even where they fall outside the mandatory scope of the ESMA Guidelines.

Implementation timeline

For AIFs and UCITS established before 16 April 2026, the RTS introduce a one-year transitional period to allow managers to update fund documentation, operational processes and technical infrastructure.

Key takeaways for AIFMs

- Fund managers managing open-ended AIFs and UCITS must ensure that each fund they manage has at least two LMTs and include them in the fund documentation.

- The RTS introduce detailed technical parameters governing the operation of LMTs.

- Existing funds benefit from a one-year transitional period following 16 April 2026.

- ESMA Guidelines, as integrated by the CSSF through Circular CSSF 26/910, provide detailed guidance on the selection, calibration and activation of LMTs, including the recommendation to combine quantitative-based tools with anti-dilution tools and the obligation for fund managers to demonstrate, at the request of the CSSF, that the calibration and activation of the selected tools are in the best interest of investors.

Conclusion

Liquidity management has traditionally been viewed as a technical aspect of portfolio management.

Under AIFMD II, it becomes a fully structured regulatory discipline. The reform aims to ensure that liquidity shocks are absorbed within the fund structure rather than transmitted to financial markets.

Share on

{kind=link}